Tesla’s (NASDAQ:TSLA) Q3 earnings are on deck this week, with the EV giant slated to release its quarterly statement on Wednesday (October 22) after the market close.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Heading into the print, Wedbush’s Daniel Ives, an analyst who ranks among the top 4% on Wall Street, notes “incremental positivity” regarding the readout, the upbeat sentiment down to a deliveries beat driven by some pull-forward EV demand ahead of the expiration of US EV tax credit and a modest recovery in China sales. “After a brutal few quarters we are finally starting to see stable demand trends for Tesla,” said the 5-star analyst. “With some Model Y refreshes abound we expect generally positive commentary around more stable demand into year-end.” That said, Ives also notes the expiration of the US EV tax credit and continued sluggish demand in Europe remain headwinds for now.

For the quarter, consensus estimates call for total revenue of around $26 billion, including about $19 billion from automotive sales – a target Ives thinks is achievable given solid performance in both EV deliveries and energy generation. Gross margins (excluding credits) are expected to continue improving from past year’s lows, while beating the expected EPS of $0.53 is not out of the question, particularly if the higher-margin energy division delivers stronger results.

While a headwind beforehand, China has now become a “source of strength,” with the Model Y fueling additional demand in the region. The new six-seat Model YL has also played a major role in attracting fresh buyers, even as more low-cost models enter the market. “Despite this tariff war playing out and changing daily, we believe that Tesla’s massive presence in China is a relatively good sign for Musk and Co. as Tesla’s Shanghai Gigafactory produces a significant amount of its global vehicles while rare earth minerals remain a crucial component for multiple products within the TSLA ecosystem (including Optimus),” Ives explained on the matter.

As for what to look out for on the earnings call, the focus will turn to Tesla’s Robotaxi rollout across the US, the production ramp for Cybercabs and Optimus expected in 2026, and updates on any new models slated for early next year. While Wednesday’s earnings and guidance will be important, Ives thinks they are likely to “take a backseat” to Tesla’s larger AI ambitions. “We continue to strongly believe the most important chapter in Tesla’s growth story is now beginning with the AI era now here,” Ives said. It begins with autonomy and then extends to robotics, with Ives believing the autonomous segment alone could be worth $1 trillion to Tesla’s valuation over the next few years – one that will start to get “unlocked over the coming months.”

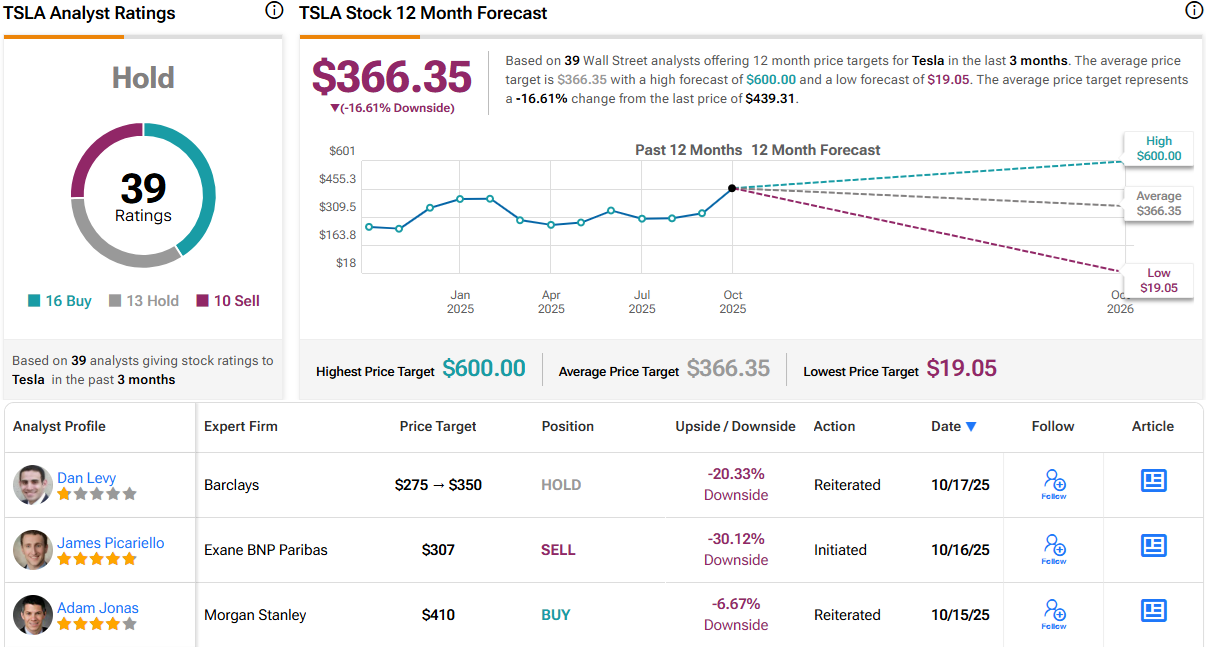

Bottom line, Ives maintained an Outperform (i.e., Buy) rating on the shares, backed by a $600 price target, implying the shares will post 12-month growth of 37%. (To watch Ives’ track record, click here)

Ives’ positive stance gets the backing of 15 other analysts, yet with an additional 13 Holds and 10 Sells, the stock only claims a Hold consensus rating. Meanwhile, the $366.35 average target implies shares will lose 17% in the months ahead. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Source link