Services are where two-thirds of consumer spending goes. And that’s where inflation is. But it’s no longer in rents.

By Wolf Richter for WOLF STREET.

The core services PCE Price Index, which excludes energy services, accelerated to +0.36% (+4.4% annualized) in July from June, the third month in a row of acceleration. The increase was driven by non-housing services; rents continued to decelerate.

This caused the 3-month core services PCE price index to accelerate to 3.1% annualized; and it caused the 6-month index to accelerate to 3.3%. Services are not tariffed.

We have already seen this trend of sharply rising services inflation in the CPI for July, and in the PPI for July, both released earlier this month. The PCE price index here is favored by the Fed as yardstick for its inflation target and usually runs lower than the CPI – and did so for July.

, Durable Goods Inflation (where Tariffs Hit) Turns Negative Month to Month")

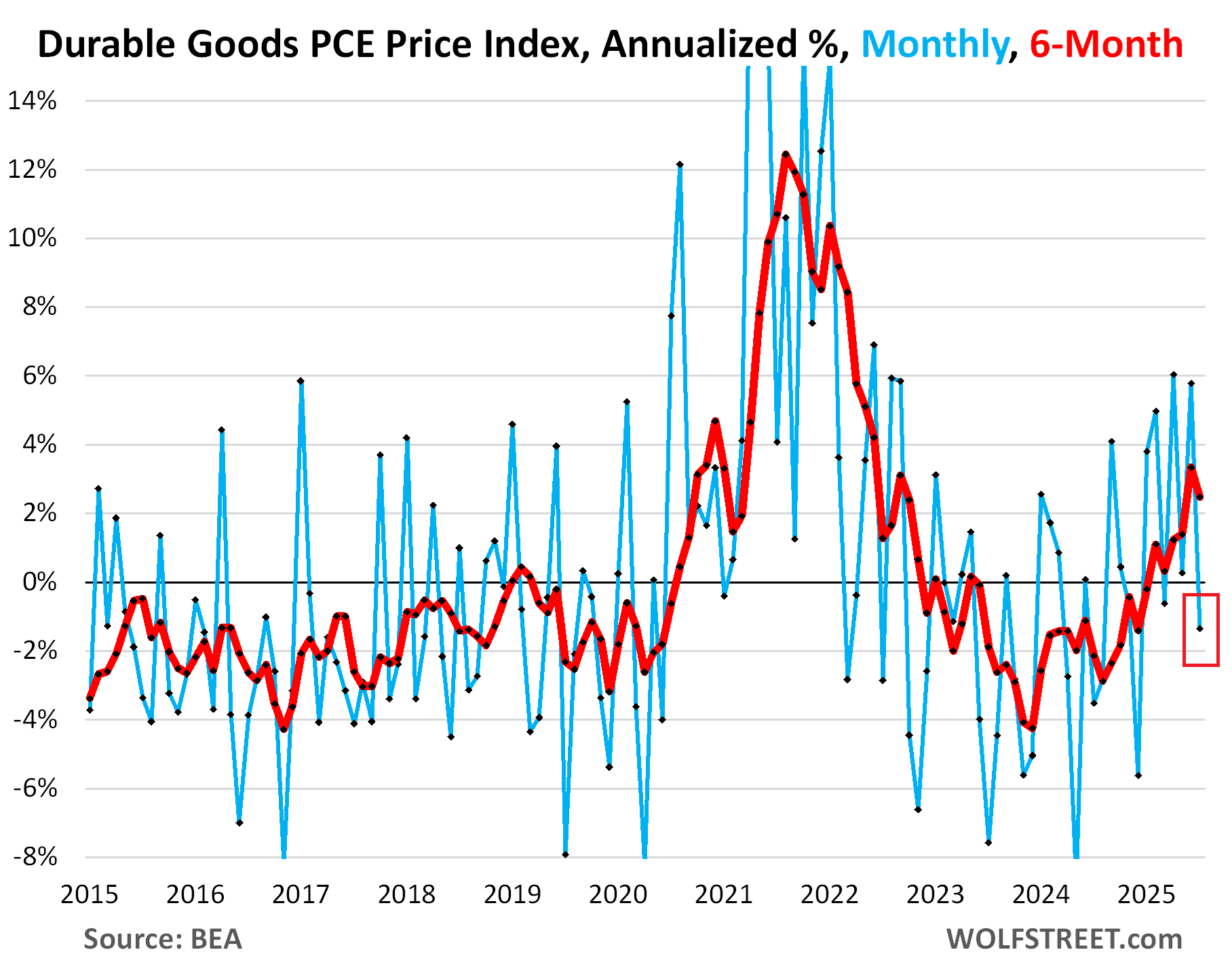

But the durable goods PCE price index fell by 0.11% (-1.3% annualized in July from June). Many durable goods are imported, or their components are imported, and many of them are tariffed.

Durable goods include all motor vehicles, appliances, furniture, bicycles, phones, audio and video equipment, etc.

This is where a big part of the tariffs would show up. But whether or not companies can pass on these taxes depends on market conditions – whether consumers keep buying products at higher prices, now that the free money is gone, or whether sales fall, and companies have to cut prices to get the sales they want.

Durable goods prices spiked massively starting in 2020 and into 2022, and then consumers came out of their pay-whatever stupor, and as resistance to higher prices set in, companies were forced to cut prices and offer deals in order to sell their goods, which is why the durable goods PCE price index turned negative in late 2022. It turned positive for much of 2025 but fell into the negative again in July.

The 6-month index decelerated to +2.5% annualized, from +3.4% in the prior month.

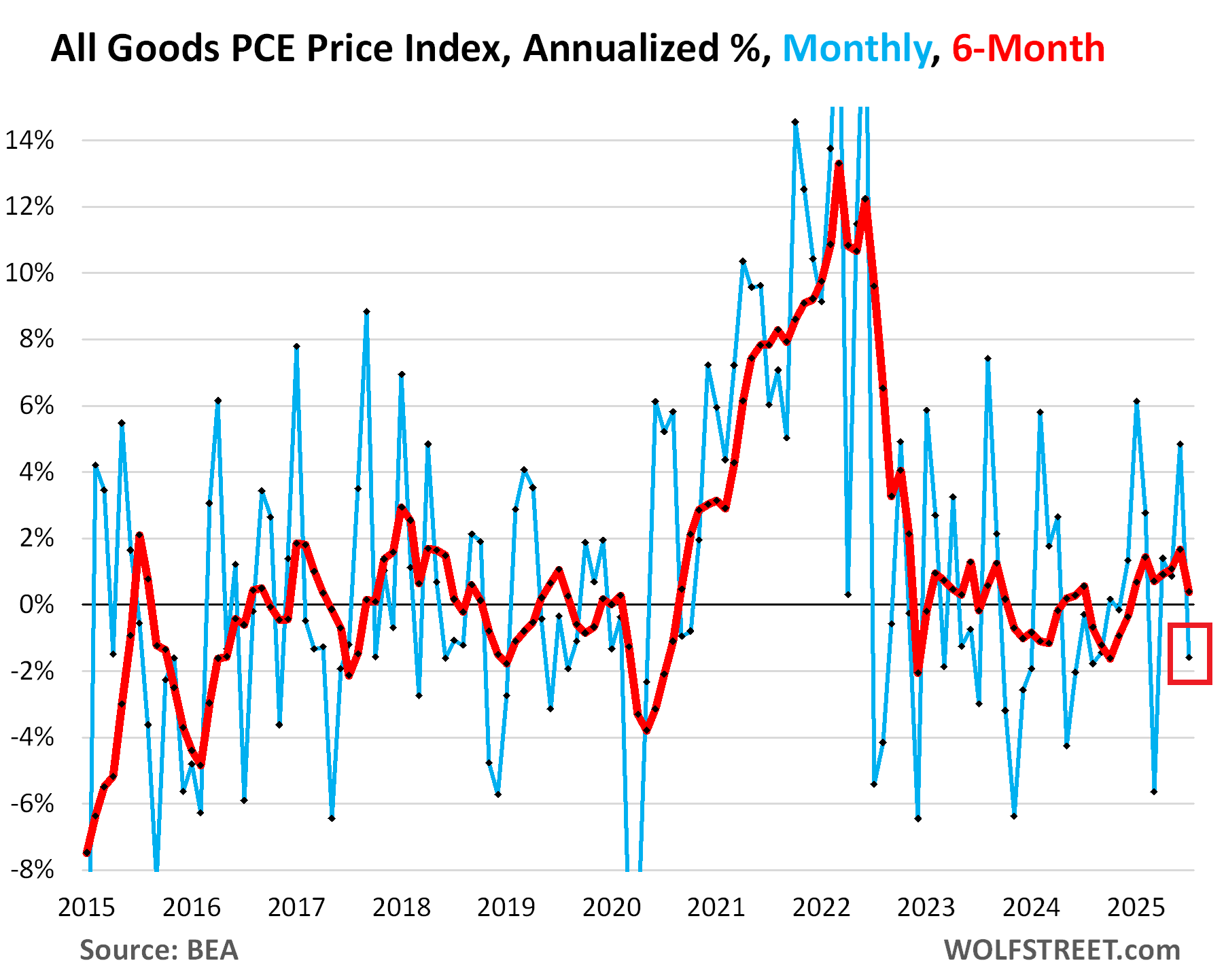

All goods inflation – durables plus nondurables such as food, gasoline, clothing, shoes, supplies, etc. – fell by 0.13% (-1.6% annualized) in July from June.

The 6-month all-goods PCE price index decelerated to +0.4% annualized.

Services inflation is where the action is. Services account for about two-thirds of consumer spending. And services inflation is very hard to squash, as we can see now.

While folks were bent over looking with their big magnifying glasses for micro-traces of tariffs in some cherrypicked goods prices, services inflation blew out behind their backs.

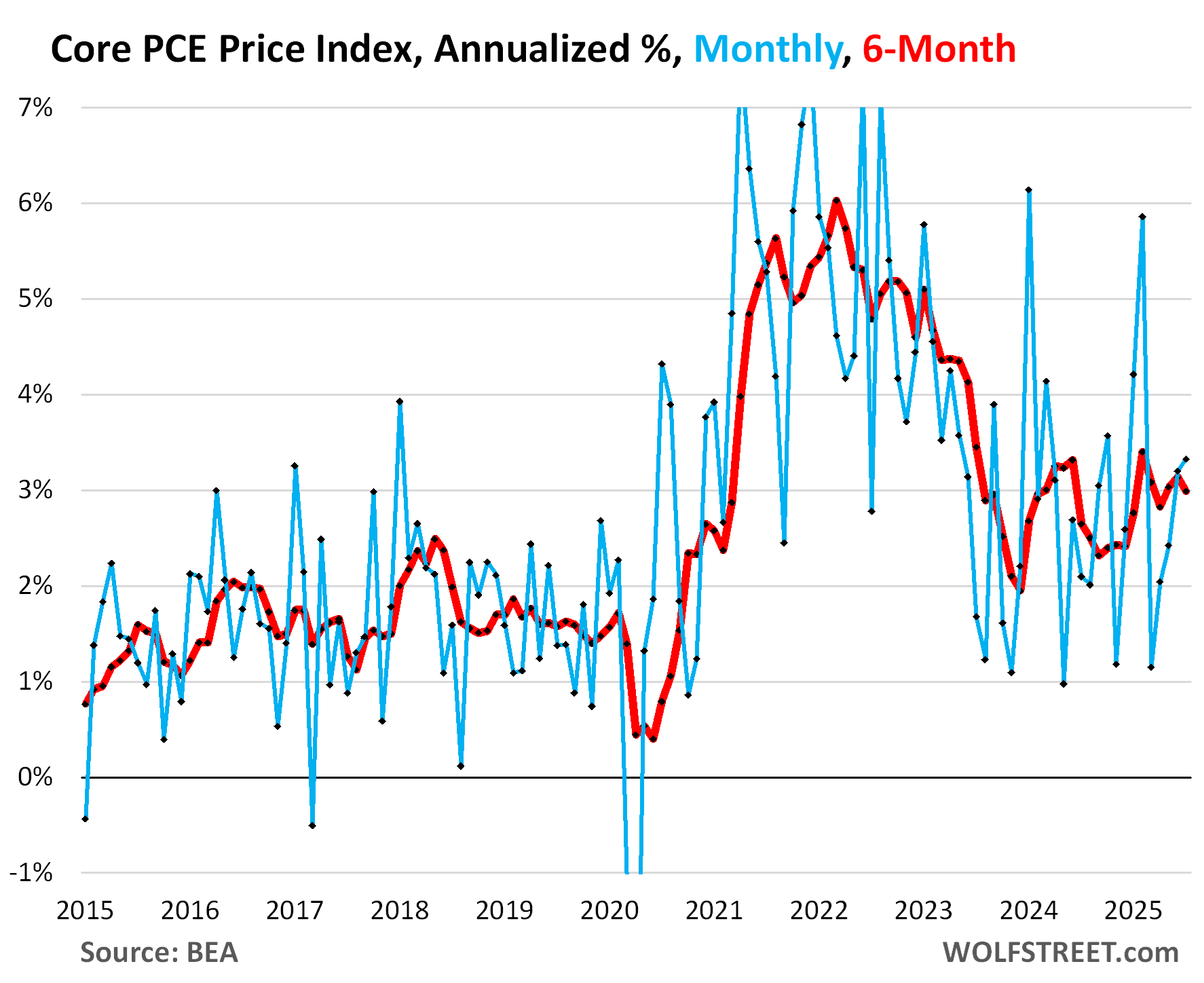

The core PCE price index accelerated a little to 0.27% (+3.3% annualized) in July from June, on this mix of much higher core services inflation and negative durable goods inflation.

The 6-month index decelerated a little to 3.0% annualized in July, from 3.1% in June.

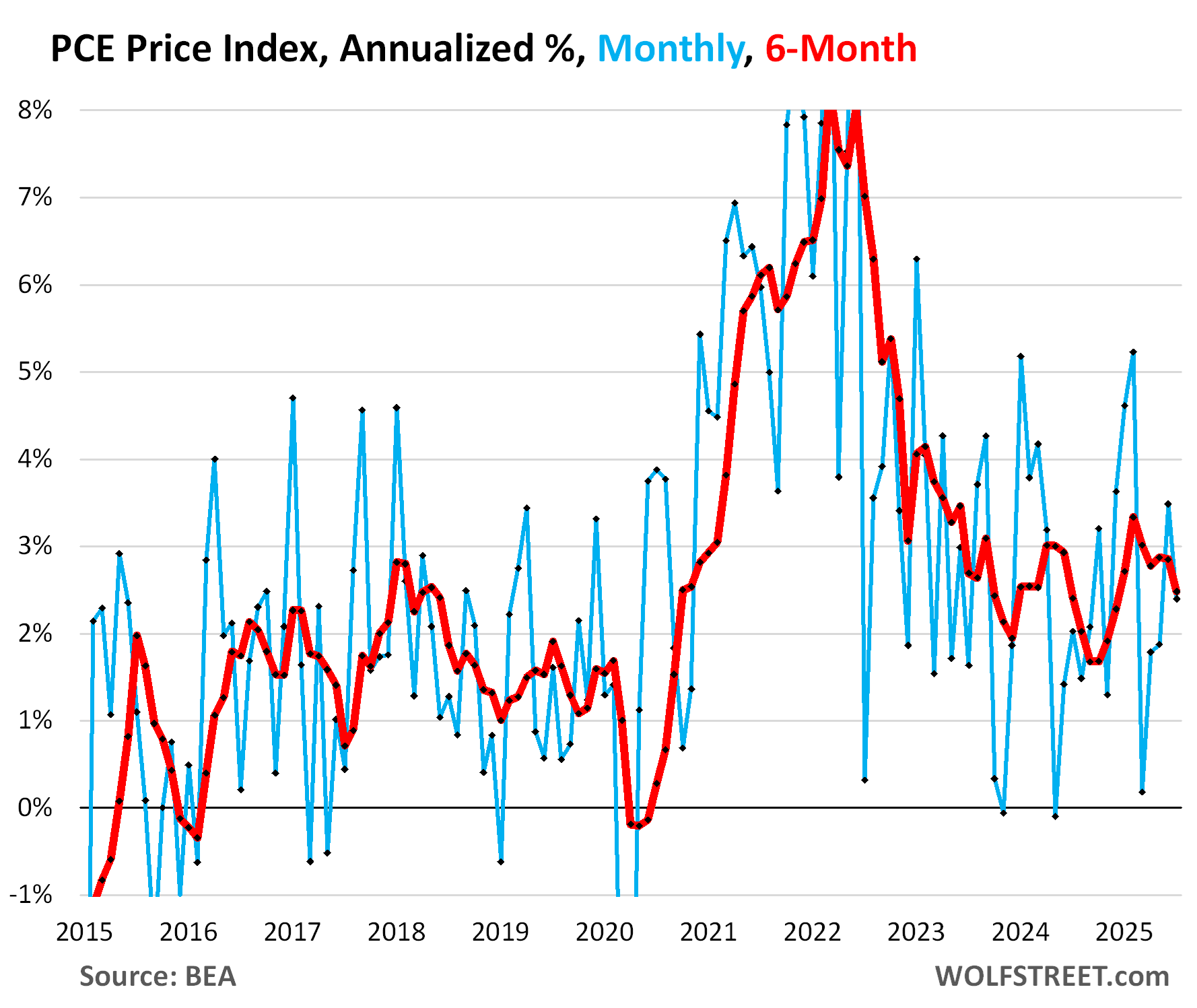

The headline PCE price index decelerated to 0.20% (+2.4% annualized) in July from June, pushed down by the continued plunge in energy prices (-1.0% not annualized) that overpowered the acceleration in core services inflation (+0.36% not annualized).

The 6-month headline index decelerated to 2.5% annualized.

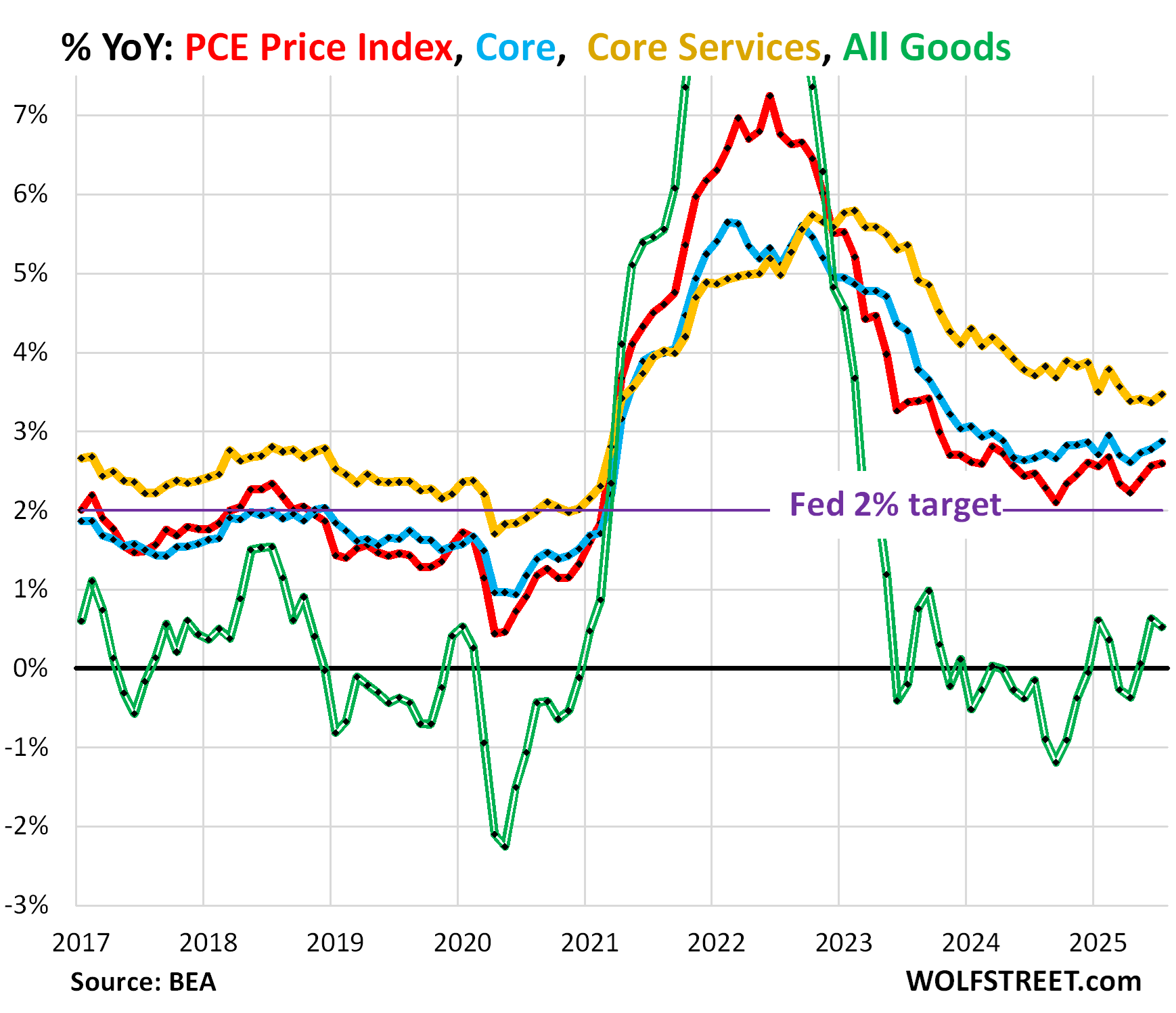

Year-over-year and the Fed’s 2% target.

The year-over-year overall PCE price index and the year-over-year core PCE price index form the yard stick that the Fed uses for its 2% inflation target. Both are well above the 2% target and moving further away from it.

In addition, core PCE and headline PCE were worse in July than they were a year ago. In other words, inflation is now worse than it was a year ago.

Headline PCE price index accelerated a hair to 2.60% in July, worse than a year ago (2.47%), and the third month of acceleration in a row (red in the chart below).

Core PCE price index accelerated to 2.88%, worse than a year ago (2.67%), and the third month of acceleration in a row (blue in the chart).

Core services PCE index accelerated to 3.47% (yellow).

Goods PCE price index decelerated to 0.52% (double green line) and remains very low.

Raising prices is tricky and profits are still huge.

All companies want to raise prices all the time. The reason they don’t is that sales plunge when they do. That is particularly true for companies selling goods, which can be easily comparison-shopped online.

But in 2021 and 2022, as free money was floating around, companies saw that they could raise prices, and by a lot, and sales didn’t plunge because consumers were willing to pay whatever.

When money is free, prices don’t matter. And that’s the phenomenon we saw at the time. But that time is over. The free money is gone. Prices matter a lot.

Whatever part of the tariffs will eventually make it into consumer prices may end up being a one-time bump in the price level of those goods.

But services prices are much harder to tamp down on, in part because many essential services are hard to comparison-shop, and because some big important services don’t have a lot, if any, competition.

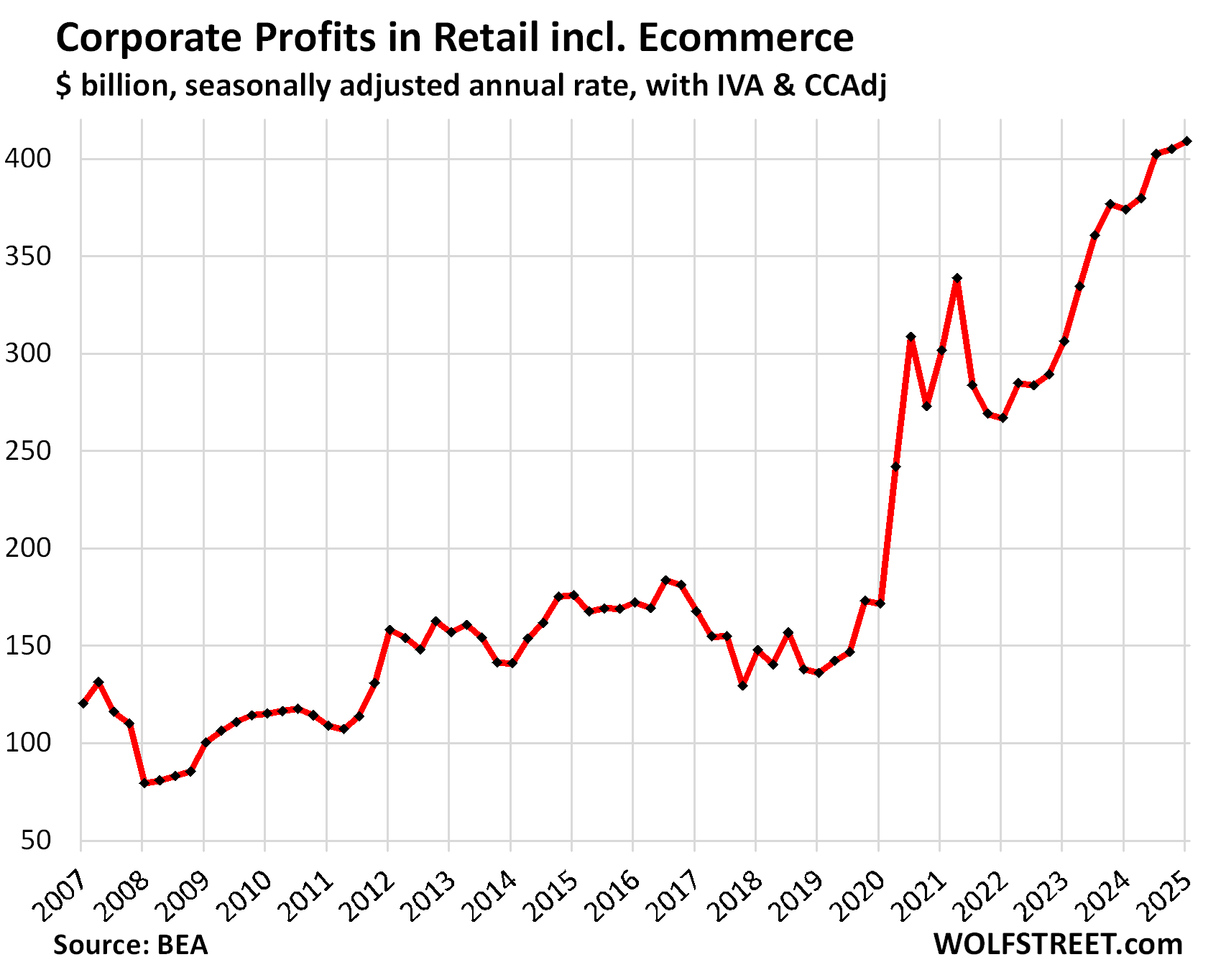

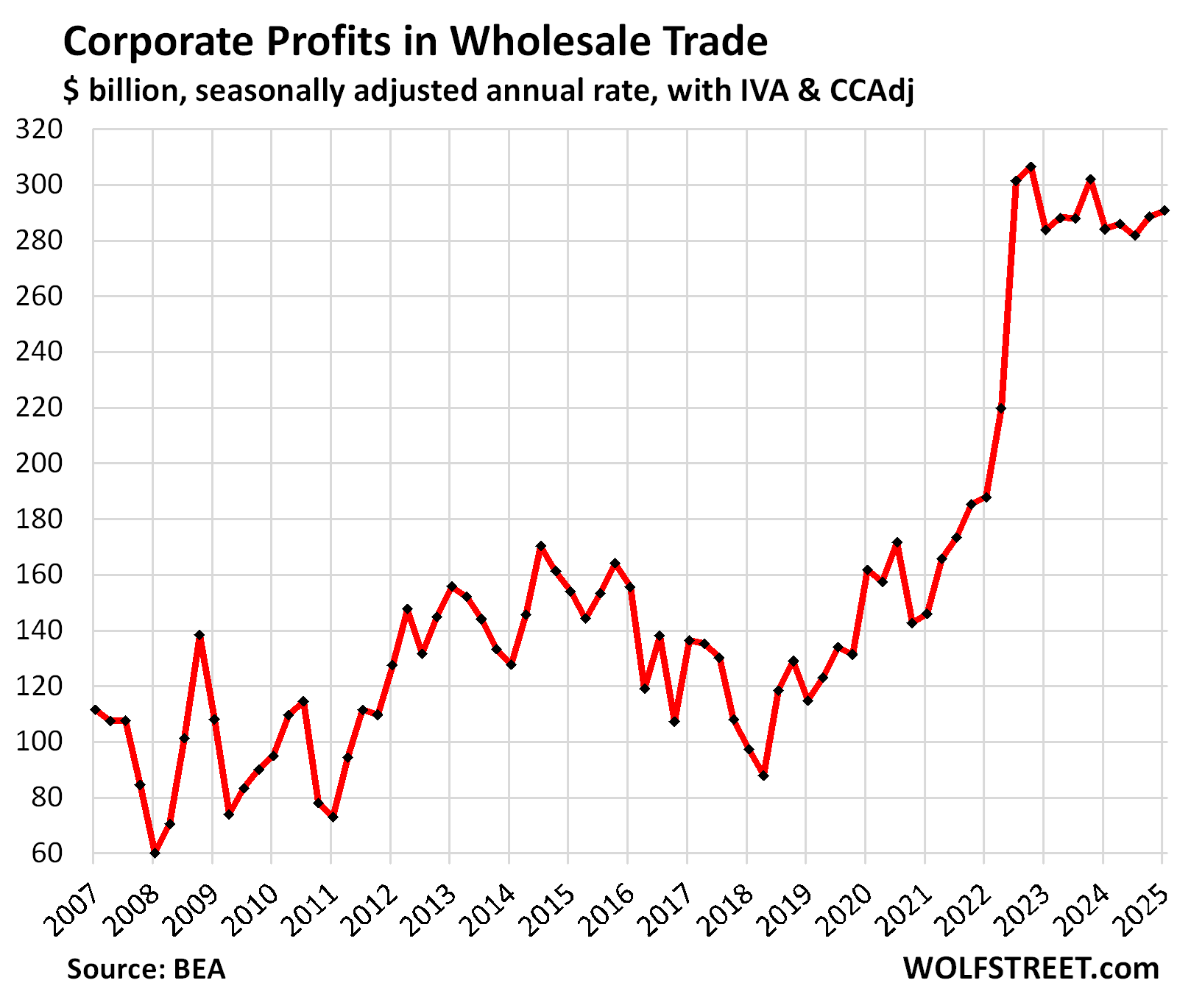

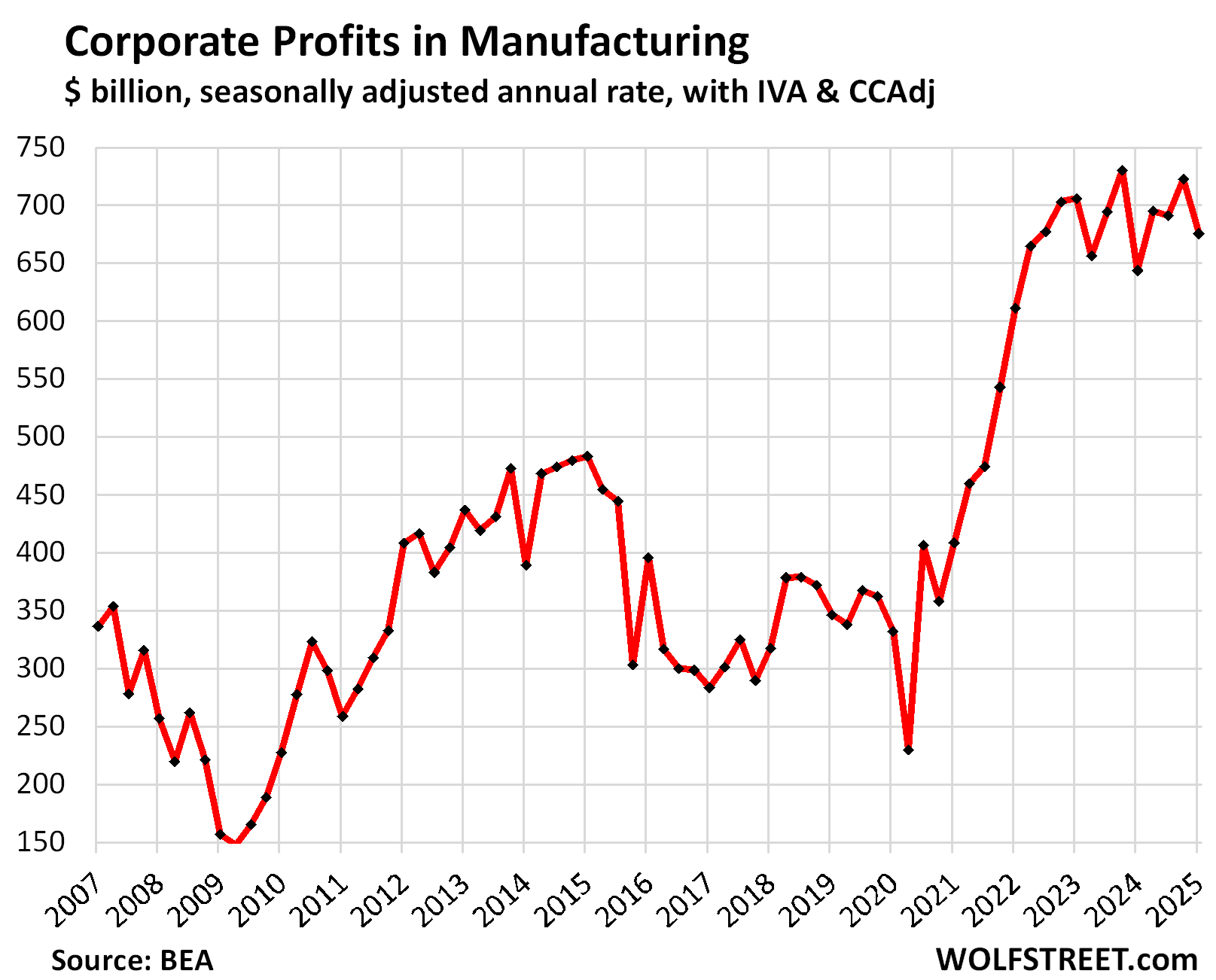

Companies now have lots of room to eat the tariffs after they jacked up their prices during the high-inflation years far more than their costs rose. We discussed the details of those profits by industry here. Some morsels from that report:

At retailers, including ecommerce, profits rose by 138% since Q1 2020:

At wholesalers, profits rose by 80% since Q1 2020:

At manufacturers, profits rose by 100% since Q1 2020:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

WOLF STREET FEATURE: Daily Market Insights by Chris Vermeulen, Chief Investment Officer, TheTechnicalTraders.com.

Source link