Month-End Liquidity-Palooza: Banks finally used the new & improved SRF the way the Fed has been exhorting them to use it to keep a lid on repo rates.

By Wolf Richter for WOLF STREET.

Dallas Fed president Lorie Logan’s speech this morning couldn’t incorporate what happened at the Fed’s new and improved Standing Repo Facility (SRF) at the auction this morning and at the auction this afternoon. But she should be pleased. Usage of the SRF, where banks can borrow from the Fed overnight at 4.0% currently, spiked to $50 billion, the highest since the SRF was established in July 2021.

“I was disappointed to see rates on a large share of tri-party repo transactions exceed the SRF rate at times this week,” she lamented the state of affairs where banks had not borrowed enough at the SRF to lend at higher rates to the repo market to quell the rising rates in the repo market.

“I anticipate that primary dealers will use the facility [the SRF] to obtain repo funding when it is economical to do so. Drawing on the SRF when the rate is economical is a sound way for a primary dealer to serve the [repo] market,” she said in the speech.

And she exhorted “dealers” – the banks that are the approved counterparties at the SRF – to borrow at the SRF and lend to the repo market when the rate spread makes this profitable for the banks because that would keep repo rates near the Fed’s policy rates.

“Dealers may now need to step up their readiness to access the SRF in response to rate moves,” she said.

And today, dealers did. She should be pleased. Today, they borrowed $20 billion at the morning auction and $30 billion at the afternoon auction at the SRF, $50 billion in total.

Spiking uptake at the SRF at month-end and quarter-end and on key tax days will become normal.

These repos are “overnight repurchase agreements” that mature the next business day (on Monday), when the Fed gets its $50 billion back and the banks get their collateral back.

If no new repos are taken out on Monday, the balance at the SRF will be zero, and the liquidity that was added on Friday is then backed out of the market. This occurred on the zero-balance days in the chart above, most recently on October 24, 22, 17, 14, 13, 12, etc.

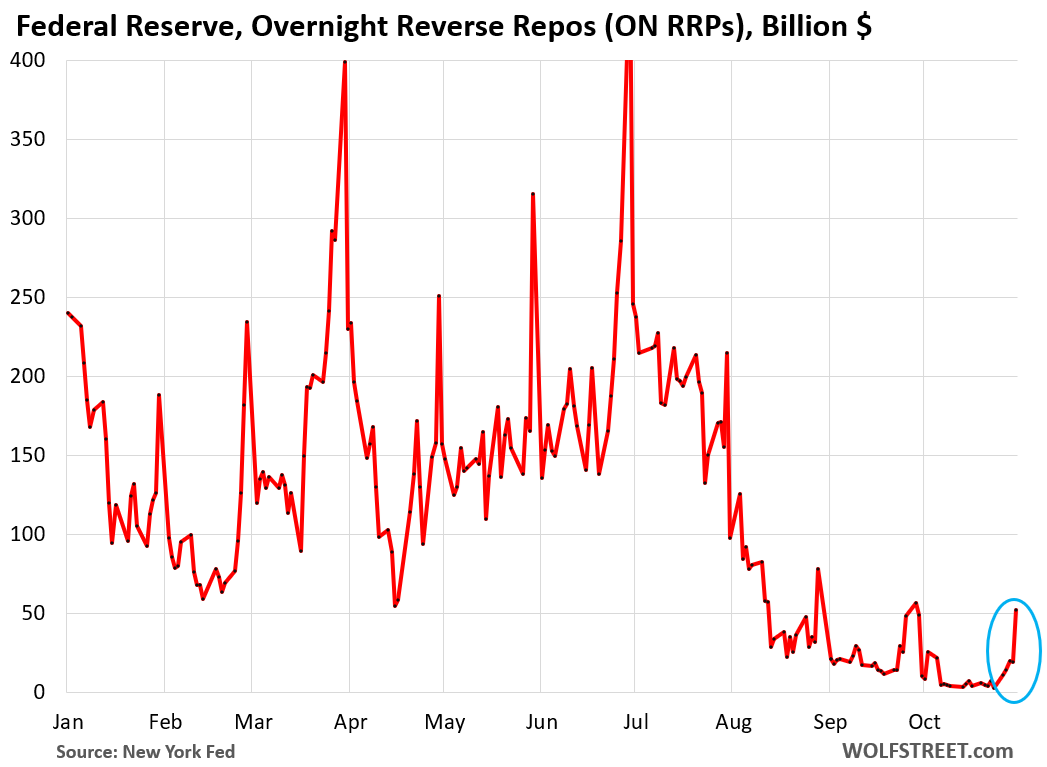

But ON RRPs also spiked to $52 billion: opposite direction.

The Fed’s Overnight Reverse Repo (ON RRP) facility is the opposite of the SRF. ON RRPs represent liquidity deposited at the Fed. The SRF represents liquidity drawn from the Fed.

ON RRPs spiked to $52 billion today. A week ago, it was essentially zero. Spiking ON RRP balances at the end of the month and at the end of the quarter have been normal, and this spike was rather small, compared to the prior spikes.

This $52 billion of ON RRPs counterbalanced the $50 billion drawn on the SRF facility today, and the net liquidity added by the Fed – so SRF balance minus ON RRP balance – was less than zero. In other words, the ON RRP facility effectively withdrew $52 billion in liquidity from the repo market, while banks borrowed $50 billion from the Fed via the SRF to supply liquidity to the market.

The $7-trillion money market fund industry is a big lender to the repo market. But money market funds can also put their extra cash on deposit at the Fed and earn 3.75% interest currently.

In early 2023, the ON RRP facility still had a balance of $2.3 trillion that QT has now largely drained from it.

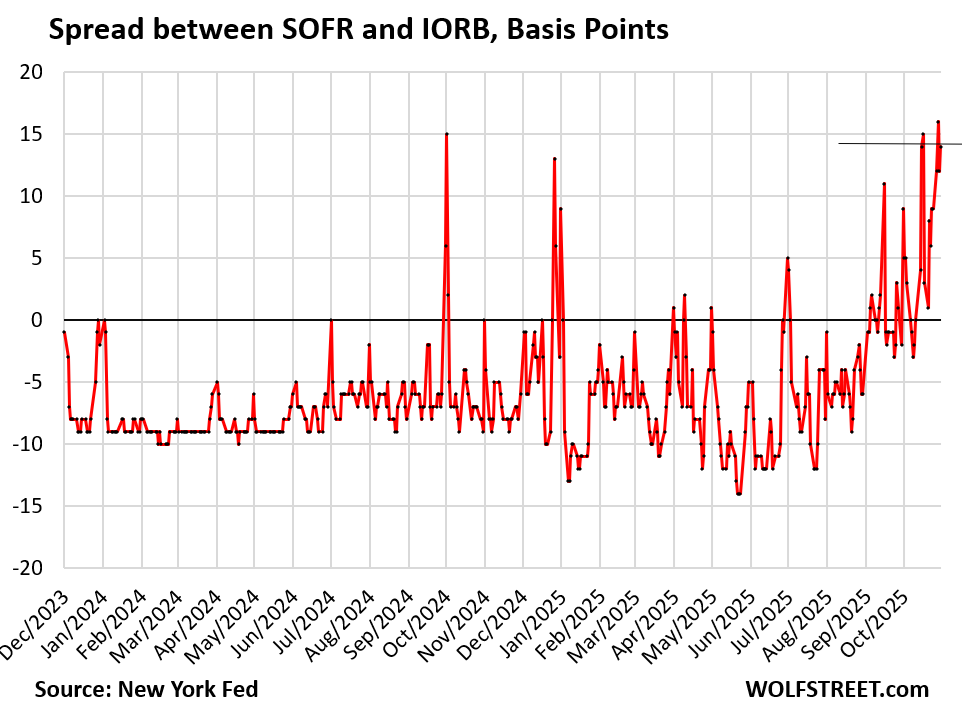

Repo rates have become volatile.

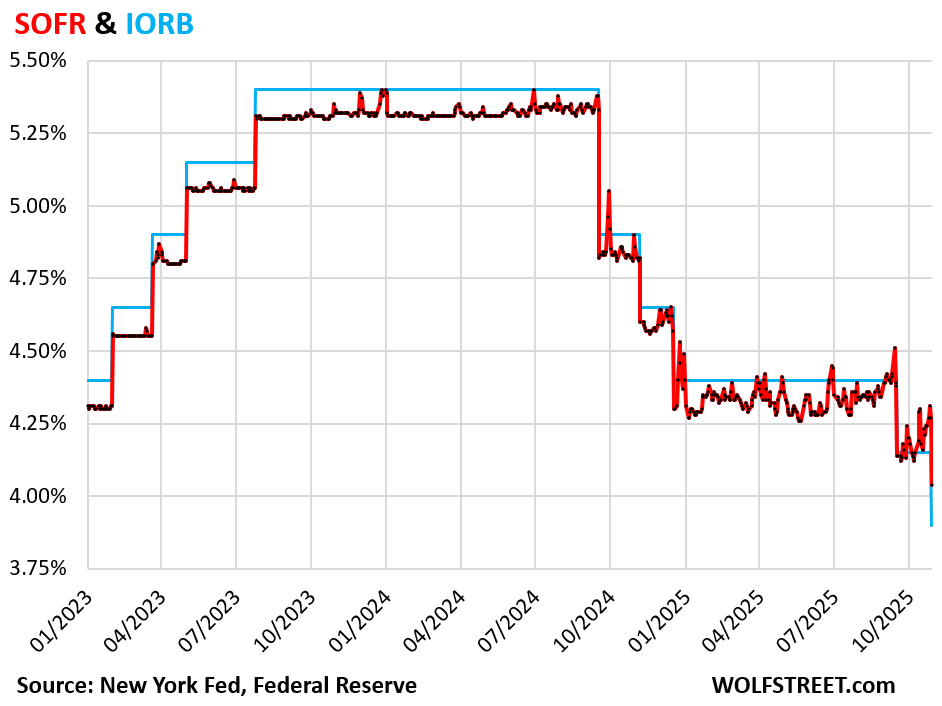

The Secured Overnight Funding Rate (SOFR), which tracks a $3-trillion-a-day segment of the repo market, has become volatile, and has risen above the interest rate that the Fed pays banks on their reserve balances (IORB), and the spread between SOFR and IORB has turned positive.

Normally, at month-end and quarter-end, when massive liquidity flows increase the pressures in the market, SOFR would spike for a day or two above IORB, and then quickly fall below it and remain below it, and the spread between SOFR and IORB would be negative.

SOFR was 4.04% on Thursday (today’s rates will be released on Monday). Intraday, repo rates ranged from 3.95% to 4.27%.

IORB was cut to 3.9% on Thursday as part of the Fed’s rate cuts announced Wednesday afternoon (blue line in the chart below). Normally SOFR (red) would be a few basis points below that. But this is month-end and tighter liquidity, and SOFR was 4.04%, so 14 basis points higher than IORB.

With SOFR at 4.04% and IORB at 3.9% on October 30, the spread between them was 14 basis points. This spread was slightly narrower than on October 28, when it reached 16 basis points.

Banks rich on reserves could lend to the repo market to profit from the spread, which may have been over 20 basis points (high end of SOFR was 4.27% on Thursday).

Banks that don’t want to use their reserves could have borrowed at the SRF at 4.0% and lend to the repo market and still make a nice spread. And they did today!

“With rates averaging higher than they were just a few months ago, the likelihood of the SRF rate becoming economical on some days is higher,” Logan said in her speech. By “economical,” she means, lower than market rates to where banks borrow at the SRF and lend at a higher rate to the repo market and profit from the spread.

And this has been happening, particularly today, when the uptake at the SRF spiked to $50 billion.

Logan cited these repo market rate and liquidity dynamics in support of the FOMC’s decision on Wednesday to end QT as of December 1.

Logan said today that the SRF should be further improved through central clearing:

“In my view, central clearing would further strengthen the facility’s effectiveness. The Fed’s counterparties could net down centrally cleared SRF borrowing against onward lending to other firms. Netting would reduce counterparties’ costs and risks of intermediating SRF funds to the broader market, helping liquidity to flow efficiently through the financial system.”

And she added:

“Streamlined SRF borrowing could be particularly helpful in the event of financial stress. Times of stress are the times when it’s most crucial for the Fed to be able to deliver the liquidity the system needs. Yet times of stress are also exactly when market participants try to de-risk their balance sheets by pulling back from intermediation.”

In her conclusion, she exhorted dealers again to make use of the SRF to lend to the repo market and thereby keep the repo rates in line and reiterated that the new and improved SRF should be further improved: “…dealers may need to increase their readiness to draw on the SRF in an environment where it is in the money more often, and the Fed should also continue to enhance the facility’s usability.”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

WOLF STREET FEATURE: Daily Market Insights by Chris Vermeulen, Chief Investment Officer, TheTechnicalTraders.com.

Source link