It’s been clear for a while that the Fed was leaning toward easier policy, and that shift is now underway. The central bank cut its benchmark interest rate by a quarter-point last week – the first move of its kind since last December. Now, all eyes are on what comes next.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

Economists expect to see additional cutting from the Fed; the consensus believes that a series of quarter-point cuts, between three and five by the end of next year, is the most likely scenario. Goldman Sachs strategist David Kostin, in his recent note, explores the ramifications of this shift in Fed policy.

“Stocks typically benefit from lower yields as long as the economic growth outlook remains solid,” Kostin says, and goes on to add, “Equities have also continued to price a resilient growth outlook, in line with our economists’ forecast. The apparent stabilization in underlying trend job growth following three months of deceleration supports this view. In addition to spurring Fed easing, another way weaker jobs data help equities is because slower wage growth should boost corporate profit margins, all else equal.”

In this environment, then, with rates coming down, investors should expect to see the stock rally continue – and Goldman’s analysts are picking out the shares that may outperform such an upwardly mobile trend. We’ve checked in with the TipRanks data and the Goldman commentaries; here’s the case for the bank’s recent picks.

Celsius Holdings (CELH)

We’ll start our look at Goldman’s picks with Celsius Holdings, a beverage company that has been in business since 2004. Celsius has several lines of energy drinks and nutrition products designed for the active lifestyle. The company’s products include its eponymous hydration beverage, as well as the Celsius Energy drink line, and two lines of powdered beverages, sold in single-drink packets, designed for easy travel before being mixed with water.

Celsius products can be found in specialty store chains, such as Campus Protein or The Vitamin Shoppe, as well as major retailers such as Target or Walmart; the products are also available on Amazon. In its 21 years in business, Celsius has built itself into the #3 energy drink product in the US, and has a fast-growing international footprint.

Earlier this year, Celsius made several announcements that demonstrate its continued expansion. In February, Celsius announced its intent to acquire the female-focused functional beverage company Alani Nu, in a transaction valued at $1.8 billion. That included $150 million in tax assets as well as a net purchase price of $1.65 billion. The companies announced in April that the transaction was completed; the purchase was conducted in cash and stock. Following the acquisition, Celsius announced an expansion of its existing partnership with Pepsi, under which the two companies will cooperate to market their beverage products in the US and Canadian markets. The Alani Nu lines will move into Pepsi’s US distribution system, while Celsius will take on Pepsi’s Rockstar Energy brand in the US and Canada. Pepsi holds an 11% ownership stake in Celsius.

Turning to the financial results, we find that Celsius generated revenues of $739.3 million in 2Q25, for an impressive year-over-year gain of 84%. The company’s revenue total was almost $85 million better than had been expected. At the bottom line, Celsius reported a non-GAAP EPS of 47 cents, beating the forecast by 23 cents per share.

Covering this stock for Goldman, consumer products expert Bonnie Herzog notes several reasons to expect Celsius to continue posting gains. Laying out the upbeat case, she writes, “We see a long runway of volume-led +DD% topline growth and margin expansion ahead for CELH given: (1) Its exposure to a very attractive energy drink category – We believe the energy drink category is one of the most attractive categories within the broader Consumer Staples industry given its strong global +HSD%/+DD% volume-driven growth… (2) Opportunities for further share gains – CELH has been a disruptor in the category over the last several years and currently holds a ~17.3% share of the U.S. energy drink category (per mgmt as of 8/7/25) – up +180bps y/y, primarily by driving incremental share for the category as well as taking share from Bang, Red Bull and MNST. While we’re cognizant that share gains for CELH will become more challenging going forward – as is evident from Celsius’ uneven share performance recently – we’re confident that CELH can continue to take share and expand the energy drink category, especially given its recent acquisition of Alani Nu.”

Herzog follows this stance with a Buy rating on the shares, and a price target of $72 that indicates a 40% upside potential for the year ahead. (To watch Herzog’s track record, click here)

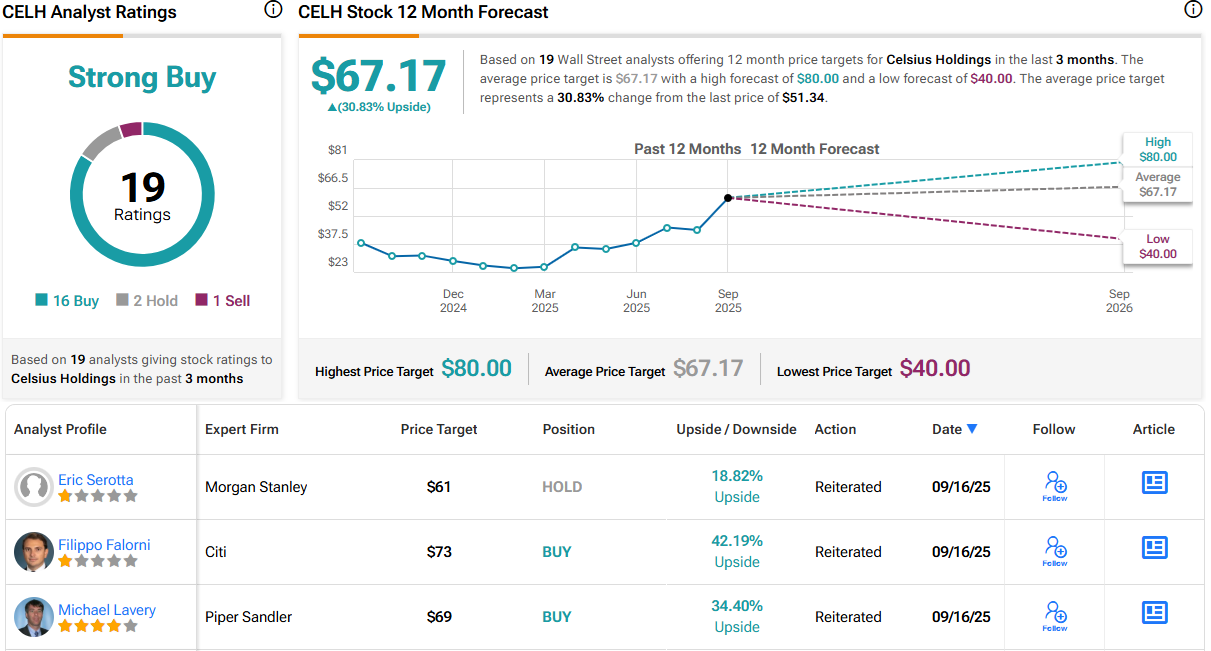

The 19 recent analyst reviews on record for CELH include 16 Buys, 2 Holds, and 1 Sell, for a Strong Buy consensus rating. The stock is currently trading for $51.34 and its $67.17 average price target implies a 12-month gain of ~31%. (See CELH stock forecast)

StepStone Group (STEP)

The second of Golman’s picks that we’ll look at is a financial services company with 19 years of experience. New York-based StepStone describes itself as a global private markets investments firm, bent on offering its clientele customized solutions for their investment needs along with sophisticated advisory and data services. The company acts as a partner for its clients, working with them to develop private market portfolios that will bring returns while meeting specific objectives in areas of private equity, private debt, real estate, and infrastructure assets.

What this means in practice is that StepStone’s 1,100-plus employees, working out of 29 offices around the world, keep their fingers on the pulse of global finance. The company holds more than $199 billion in assets under management and claims ‘total capital responsibility’ for $723 billion. The firm’s approach is shaped by market-leading proprietary research and data analysis, tailored to enhance decision making, risk analysis, and portfolio forecasting.

In recent quarters, StepStone has seen a sharp increase in its revenues. For the fiscal year 2025, which ended this past March 31, the company reported a top line of $1.17 billion; this marked a 65% increase over fiscal year 2024.

In the most recent quarterly release, for fiscal 1Q26, StepStone continued posting strong top-line gains. The company’s revenue came in at $364.3 million, for a 95% year-over-year increase. On net income, the company posted a loss for the quarter of 49 cents per share.

Goldman’s Alexander Blostein is impressed by this financial advisor’s fast growth, and in his coverage of the stock the 5-star analyst explains why that growth should continue to power gains.

“We see STEP as one of the fastest growing Alt managers with a 24% Normalized FRE CAGR from 2024-2028E (22% overall EPS CAGR), supported by its robust and fast growing Private Wealth business, strong flagship fundraising cycle with numerous Secondaries funds raising, and $29bn of Shadow AUM driving SMA growth,” Blostein said. “In particular, we see STEP’s Private Wealth AUM reaching ~$33bn by 2028, with a 67% 2025-2028E management fee CAGR and additional contribution from Fee-Related Performance revenues amid robust product line-up, unique structure and diverse distribution. While economics in the Private Wealth business are currently shared with Private Wealth employees via a revenue share (NCI) structure, STEP has a call option in 3Q27 to buy out the NCI which we estimate will be meaningfully accretive at +42%/24% to FRE/EPS in 2028E. We believe this dynamic is underappreciated by the markets.”

Blostein rates STEP as a Buy, and he complements that with an $83 price target that suggests a one-year upside for the stock of 24%. (To watch Blostein’s track record, click here)

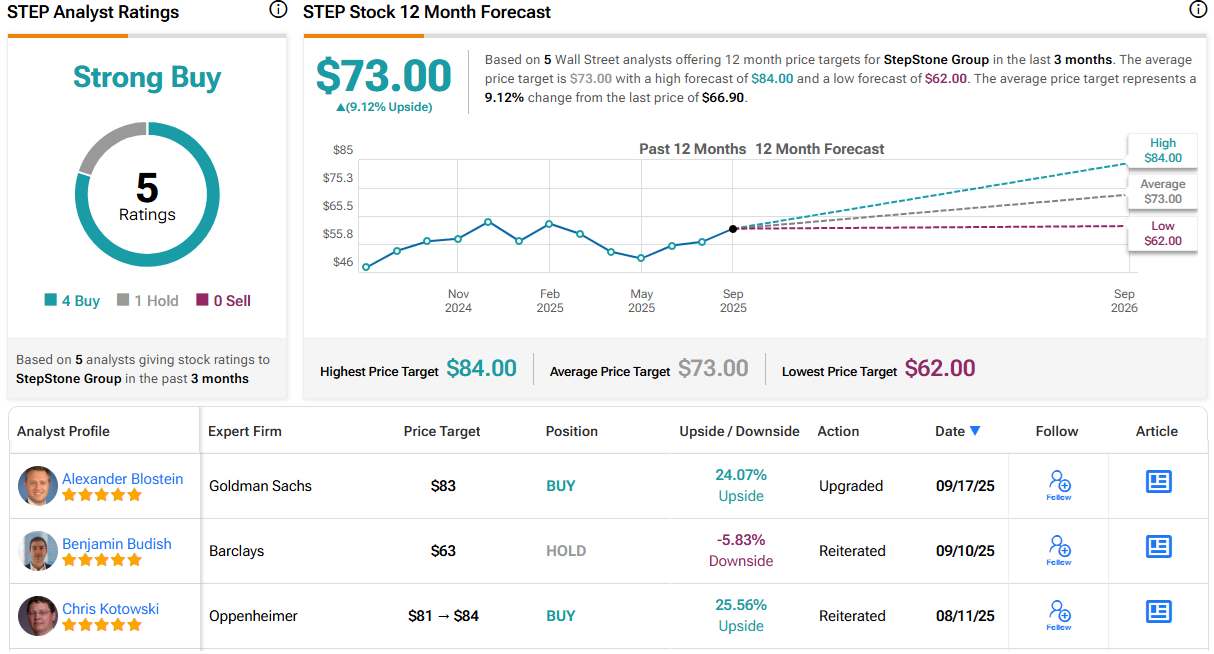

The 5 recent analyst reviews here split 4 to 1 in favor of Buys over Holds, for a Strong Buy consensus rating. The shares are selling now for $66.90 and the $73 average price target indicates room for a 9% gain in the next 12 months. (See STEP stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

Source link

:max_bytes(150000):strip_icc()/GettyImages-2229095597-8042c1c111df4e978c5bb19182581227.jpg "Gold Is Pricier Than Ever. Here’s Why Experts See It Rising Even Higher")